Thailand’s Reform Debate Reflects a Larger Fight Over Economic Dependence on China

Bangkok is weighing deregulation, foreign investment liberalization, and industrial modernization as it tries to revive growth and reduce strategic exposure to an increasingly China-centered economy.

SYSTEM-DRIVEN

Thailand’s debate over economic reform is fundamentally about whether the country can rebuild long-term competitiveness before deepening dependence on China becomes structurally irreversible.

The immediate trigger is a growing push inside Thailand for liberalization measures aimed at attracting more Western and Japanese investment, easing restrictions on foreign businesses, and modernizing an economy that has underperformed most major Southeast Asian peers for years.

What is confirmed is that Thailand’s government has recently discussed reducing regulatory barriers for foreign firms, simplifying import rules, loosening labor restrictions affecting expatriate hiring, and accelerating industrial investment policies tied to semiconductors, advanced manufacturing, logistics, and digital infrastructure.

The reforms are being framed as economic modernization.

But the deeper strategic issue is geopolitical exposure.

China is now Thailand’s largest trading partner and one of its most influential economic actors.

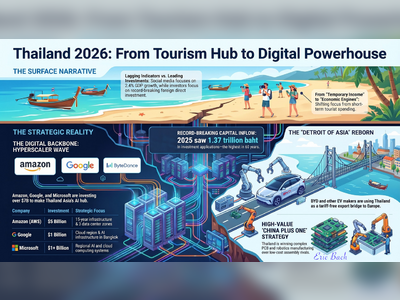

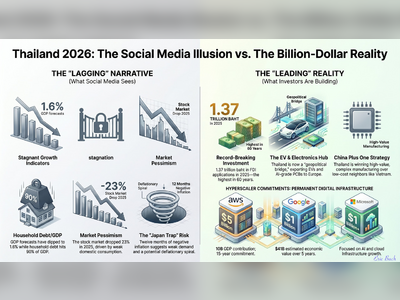

Chinese investment has expanded rapidly across electric vehicles, batteries, industrial estates, rail infrastructure, e-commerce, tourism, renewable energy, and consumer technology.

Chinese manufacturers increasingly dominate major supply chains operating inside Thailand.

That integration has delivered benefits.

Chinese capital has supported industrial expansion, tourism recovery, and infrastructure financing at a time when Thailand’s growth has weakened.

Chinese electric-vehicle manufacturers have established major production operations in Thailand, helping position the country as a regional EV hub.

But the same integration has created vulnerabilities.

Thailand’s economy has struggled with weak productivity growth, aging demographics, high household debt, stagnant wages, uneven education outcomes, and prolonged political instability.

Growth has consistently lagged behind regional competitors such as Vietnam and Indonesia.

The key issue is that Thailand risks becoming more dependent on externally driven industrial activity without upgrading its own economic structure.

That concern has intensified as global supply chains reorganize around geopolitical competition between the United States and China.

Multinational companies are increasingly pursuing “China plus one” strategies that diversify manufacturing into Southeast Asia.

Thailand wants to benefit from that shift, but it faces fierce competition from Vietnam, Malaysia, and India.

Supporters of reform argue Thailand still possesses major advantages: established automotive supply chains, strong logistics infrastructure, deep industrial expertise, geographic positioning, and relatively sophisticated manufacturing capacity.

They argue the country’s main problem is not lack of potential but institutional inertia.

Foreign businesses have long complained about restrictive ownership rules, complicated licensing systems, slow regulatory approvals, inconsistent policymaking, and protectionist structures favoring entrenched domestic interests.

Some proposed reforms target precisely those bottlenecks.

Liberalization advocates want easier visa access for skilled foreign workers, fewer restrictions on foreign corporate ownership, faster customs procedures, expanded digital infrastructure, and greater support for technology-intensive industries.

The semiconductor sector has become a major focus.

Thailand is actively seeking chip-related investment as global technology companies diversify production away from concentrated China-based manufacturing networks.

The government has promoted Thailand as a stable manufacturing platform for electronics, data centers, and power-management chips tied to electric vehicles and industrial systems.

The stakes extend beyond economics.

Thailand has historically balanced relationships among major powers while avoiding rigid alignment.

But economic dependence changes diplomatic leverage over time.

As China’s role inside Thailand’s economy expands, Bangkok faces growing pressure to manage relations carefully across trade, investment, tourism, security, and regional diplomacy.

At the same time, Thailand cannot simply detach from China.

The two economies are deeply interconnected.

Chinese tourists remain critical to Thailand’s tourism industry.

Chinese factories are embedded in Thai manufacturing networks.

Chinese imports supply industrial inputs across multiple sectors.

That reality means the current debate is less about separating from China than about restoring strategic balance.

The United States and Japan remain major investors in Thailand, particularly in advanced manufacturing and technology sectors.

Thai policymakers increasingly view diversified foreign investment as essential to preserving economic resilience and avoiding overconcentration in any single geopolitical sphere.

Domestic politics complicate reform efforts.

Thailand has experienced repeated cycles of political disruption, military intervention, constitutional conflict, and leadership turnover over the past two decades.

Businesses and investors frequently cite policy unpredictability as a major obstacle to long-term planning.

Entrenched economic structures also resist change.

Large conglomerates and politically connected interests benefit from parts of the current regulatory system.

Reforming labor rules, competition policy, licensing systems, and protected sectors could create domestic political resistance.

Meanwhile, Thailand faces mounting pressure from external shocks.

Global trade fragmentation, rising protectionism, slowing Chinese growth, and geopolitical tensions have increased uncertainty for export-dependent economies across Southeast Asia.

The practical consequence is that Thailand’s reform debate is no longer abstract.

It is becoming a direct test of whether the country can reposition itself as a diversified high-value economy rather than drift into prolonged low-growth dependence tied disproportionately to Chinese industrial and financial influence.

The next phase is likely to focus on whether Bangkok can convert reform rhetoric into measurable policy execution, particularly in foreign investment liberalization, technology upgrading, industrial competitiveness, and regulatory modernization.

Thailand’s debate over economic reform is fundamentally about whether the country can rebuild long-term competitiveness before deepening dependence on China becomes structurally irreversible.

The immediate trigger is a growing push inside Thailand for liberalization measures aimed at attracting more Western and Japanese investment, easing restrictions on foreign businesses, and modernizing an economy that has underperformed most major Southeast Asian peers for years.

What is confirmed is that Thailand’s government has recently discussed reducing regulatory barriers for foreign firms, simplifying import rules, loosening labor restrictions affecting expatriate hiring, and accelerating industrial investment policies tied to semiconductors, advanced manufacturing, logistics, and digital infrastructure.

The reforms are being framed as economic modernization.

But the deeper strategic issue is geopolitical exposure.

China is now Thailand’s largest trading partner and one of its most influential economic actors.

Chinese investment has expanded rapidly across electric vehicles, batteries, industrial estates, rail infrastructure, e-commerce, tourism, renewable energy, and consumer technology.

Chinese manufacturers increasingly dominate major supply chains operating inside Thailand.

That integration has delivered benefits.

Chinese capital has supported industrial expansion, tourism recovery, and infrastructure financing at a time when Thailand’s growth has weakened.

Chinese electric-vehicle manufacturers have established major production operations in Thailand, helping position the country as a regional EV hub.

But the same integration has created vulnerabilities.

Thailand’s economy has struggled with weak productivity growth, aging demographics, high household debt, stagnant wages, uneven education outcomes, and prolonged political instability.

Growth has consistently lagged behind regional competitors such as Vietnam and Indonesia.

The key issue is that Thailand risks becoming more dependent on externally driven industrial activity without upgrading its own economic structure.

That concern has intensified as global supply chains reorganize around geopolitical competition between the United States and China.

Multinational companies are increasingly pursuing “China plus one” strategies that diversify manufacturing into Southeast Asia.

Thailand wants to benefit from that shift, but it faces fierce competition from Vietnam, Malaysia, and India.

Supporters of reform argue Thailand still possesses major advantages: established automotive supply chains, strong logistics infrastructure, deep industrial expertise, geographic positioning, and relatively sophisticated manufacturing capacity.

They argue the country’s main problem is not lack of potential but institutional inertia.

Foreign businesses have long complained about restrictive ownership rules, complicated licensing systems, slow regulatory approvals, inconsistent policymaking, and protectionist structures favoring entrenched domestic interests.

Some proposed reforms target precisely those bottlenecks.

Liberalization advocates want easier visa access for skilled foreign workers, fewer restrictions on foreign corporate ownership, faster customs procedures, expanded digital infrastructure, and greater support for technology-intensive industries.

The semiconductor sector has become a major focus.

Thailand is actively seeking chip-related investment as global technology companies diversify production away from concentrated China-based manufacturing networks.

The government has promoted Thailand as a stable manufacturing platform for electronics, data centers, and power-management chips tied to electric vehicles and industrial systems.

The stakes extend beyond economics.

Thailand has historically balanced relationships among major powers while avoiding rigid alignment.

But economic dependence changes diplomatic leverage over time.

As China’s role inside Thailand’s economy expands, Bangkok faces growing pressure to manage relations carefully across trade, investment, tourism, security, and regional diplomacy.

At the same time, Thailand cannot simply detach from China.

The two economies are deeply interconnected.

Chinese tourists remain critical to Thailand’s tourism industry.

Chinese factories are embedded in Thai manufacturing networks.

Chinese imports supply industrial inputs across multiple sectors.

That reality means the current debate is less about separating from China than about restoring strategic balance.

The United States and Japan remain major investors in Thailand, particularly in advanced manufacturing and technology sectors.

Thai policymakers increasingly view diversified foreign investment as essential to preserving economic resilience and avoiding overconcentration in any single geopolitical sphere.

Domestic politics complicate reform efforts.

Thailand has experienced repeated cycles of political disruption, military intervention, constitutional conflict, and leadership turnover over the past two decades.

Businesses and investors frequently cite policy unpredictability as a major obstacle to long-term planning.

Entrenched economic structures also resist change.

Large conglomerates and politically connected interests benefit from parts of the current regulatory system.

Reforming labor rules, competition policy, licensing systems, and protected sectors could create domestic political resistance.

Meanwhile, Thailand faces mounting pressure from external shocks.

Global trade fragmentation, rising protectionism, slowing Chinese growth, and geopolitical tensions have increased uncertainty for export-dependent economies across Southeast Asia.

The practical consequence is that Thailand’s reform debate is no longer abstract.

It is becoming a direct test of whether the country can reposition itself as a diversified high-value economy rather than drift into prolonged low-growth dependence tied disproportionately to Chinese industrial and financial influence.

The next phase is likely to focus on whether Bangkok can convert reform rhetoric into measurable policy execution, particularly in foreign investment liberalization, technology upgrading, industrial competitiveness, and regulatory modernization.